Get rid of ads & unlock exclusive premium content

Go premium

Join our growing community:

Kenyans to pay more than double, Tourists to pay upto Sh11,000 to enter national parks from October 1 as KWS revises entry fees

Remittances from Australia to Kenya overtake Saudi Arabia and Germany

Why emerging markets will beat developed economies in 2025

Liberia Bans The Export Of Raw Rubber, To Stop Giving Away It's Wealth

Pepe, Remittix and Uniswap: The Best Crypto To Buy As Ethereum Price Targets New Highs

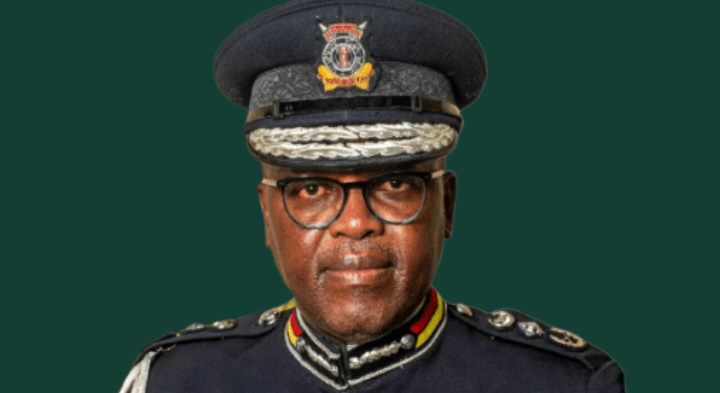

DIG Eliud Lagat earns over Ksh 650,000 monthly

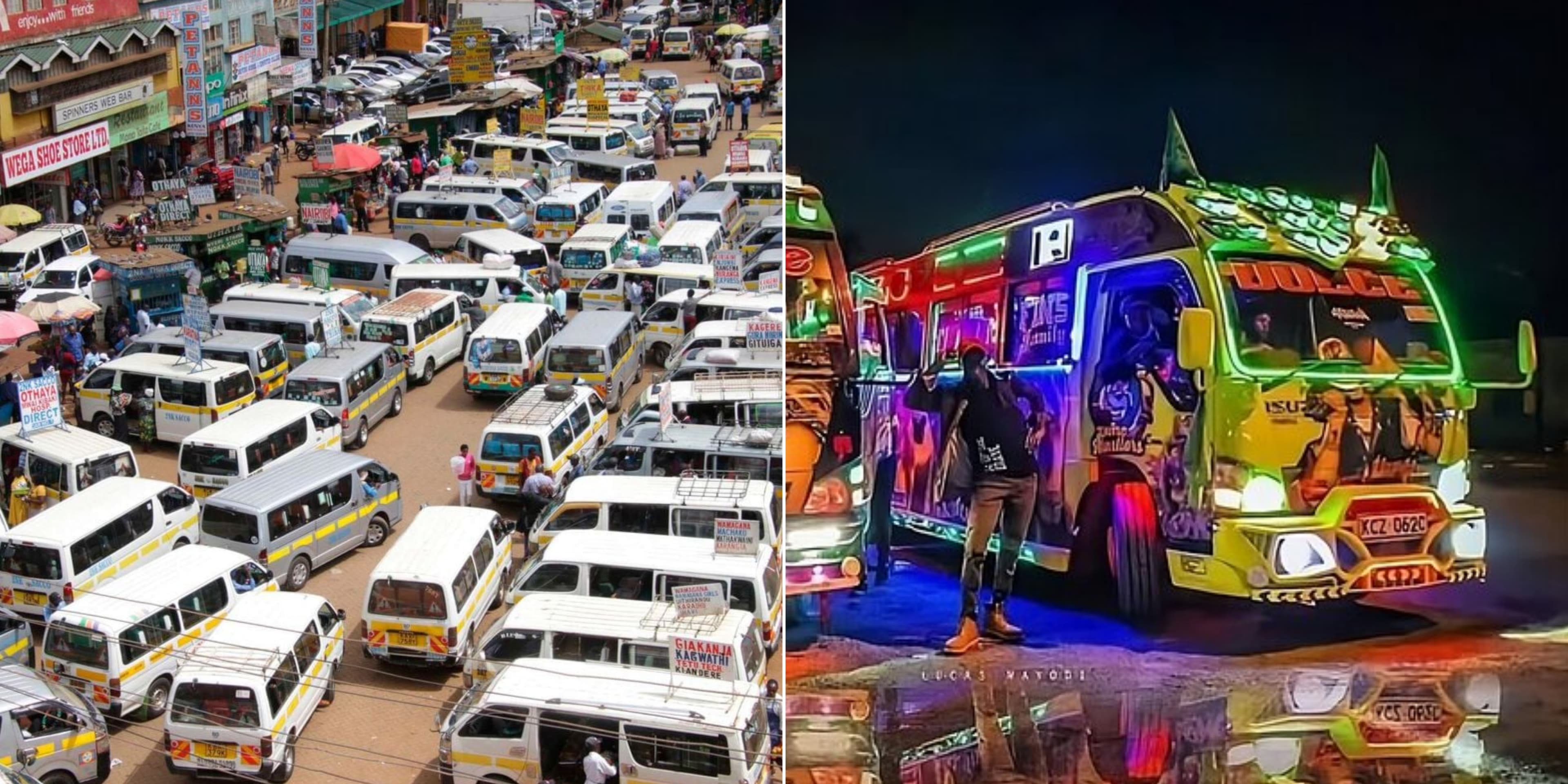

A Comprehensive Guide : How to Open a Matatu SACCO in Kenya